Planning your financial future with your partner is like rowing a boat: It’s much easier if you both agree on the direction you’d like to travel.

According to a 2024 Fidelity Investments survey, 34% of couples say they disagree on their next financial goal. And six in ten couples say they share the same vision for retirement.

Combining finances can greatly accelerate your financial progress, but only if you’re aligned on your financial goals. Getting on the same page as your partner doesn’t need to be a daunting process.

In this post, we’ll share some tips and templates backed by studies and conversations with financial advisors — so you can make sure you and your partner are on the right side of those statistics.

First, Know Yourself

While discussing goals with your partner can help inspire, it helps to have an idea of your own personal priorities and idiosyncrasies.

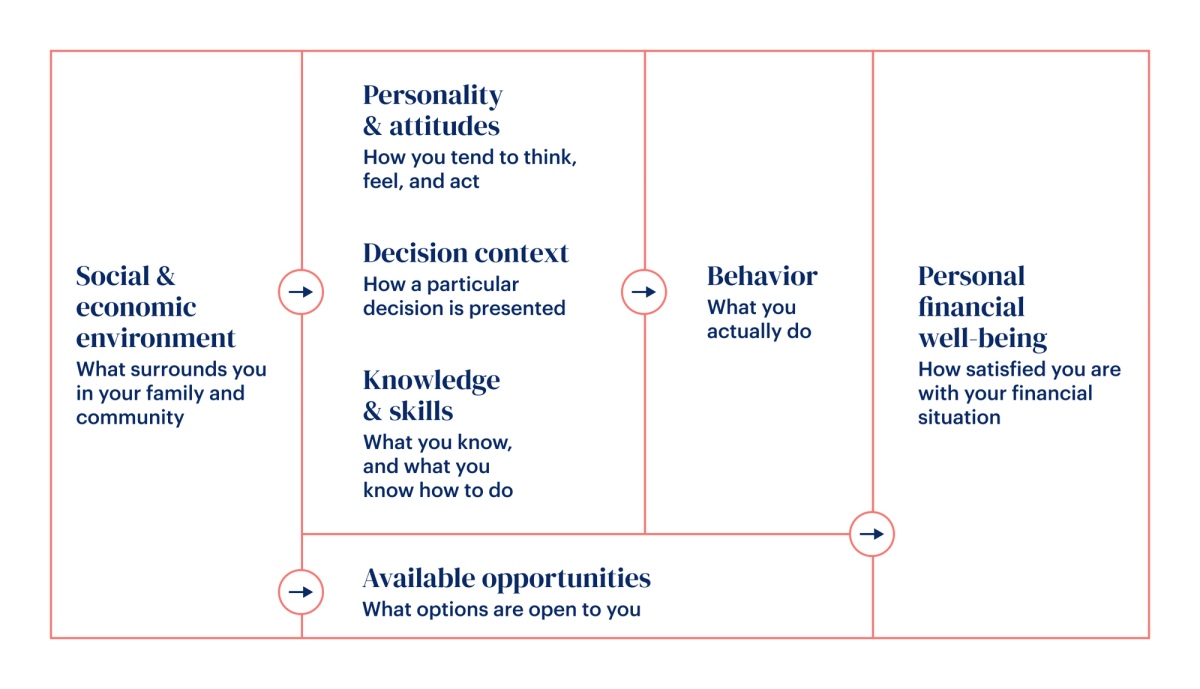

Your money beliefs are informed by things that don’t seem to have much to do with money at first. The Consumer Financial Protection Bureau has a helpful framework for taking stock of all of the factors that go into our feelings about money — a mix of our upbringing, knowledge, behavior, and available resources.

From the CFPB:

"… people arrive at adulthood with their financial personae already defined. To the extent that this is true, the behaviors, habits, and attitudes developed in youth, whether positive or negative, appear to strongly affect adult financial well-being."

Some steps you can take to take an inventory of your own goals and beliefs:

- Start with some sort of money personality diagnostic or test (like 5moneypersonalities.com) to determine some of your psychological tendencies.

- Write down your 1, 5, and 10 year goals. Be specific. “Be financially secure” is too nebulous. But “Have a six-month emergency fund” is actionable.

“When a couple comes to me and says they want to share finances together, my first step is unpacking their individual goals and priorities because they are not always aligned,” says Jonathan Wong, Founder and Certified Financial Planner of Layari Financial.

How to Set Goals You’ll Actually Achieve

With your own goals in hand, get together with your partner to explore where there are overlaps and what goals you can set together.

“It's complicated and we’re not always equipped to handle all of these conversations. But if you don’t have the conversations, it can lead to one or both of you getting overwhelmed and stuck,” says Julia Lily, founder of Ryerson Financial. “Have fun with the process of dreaming about your financial future! Shared objectives lead to more enjoyment.”

There are several popular goal setting structures (including OKRs, GROW, WOOP) — but we suggest SMART goals. SMART goals are:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Bad goal | Smart goal |

I want a new car. | We will purchase a 2023 Tesla Model 3 for $35,000 before December 15th. |

We want to travel more. | We will set aside $20,000 to travel twice a year, one international trip and one domestic trip. We’ll aim for a week for each trip. |

I want to get ahead and get out of debt | We will apply 10% of our take home pay to paying down our credit cards. We’ll be on pace to pay off the balance in 6 months. |

Some advice that may help when dreaming up you financial goals:

Don’t be afraid to think big: The goal is to create a discussion making framework for deciding how to move forward. If you both agree that spending on health is the most important thing, you can protect that gym membership spending. Or if you decide that fulfilling a life-long dream of traveling to New Zealand is important, you can weigh that when comparing your savings for that trip versus, say, adding an addition to your home.

Beware of “moral licensing”:This is when you “borrow” against future positive outcomes. For example, you know you are going to work out tomorrow so you can enjoy some extra cookies tonight. Celebrating milestones are important, but try to avoid celebrating the eventual completion of a goal.

Enjoy the process: A 2012 study found that when your motivation is “experiential” and you actually intrinsically enjoy the activity, you are more likely to stick with it. Setting goals with your partner should be a fun way to step outside of your day-to-day conversations and explore your future together.

Attach your goals to specific (and reachable) dates and times: Sure your ultimate goal may be to retire in 30 years, but be sure to have some tangible benchmarks along the way to keep yourself motivated. Remember the “T” in SMART is for “Time Bound.”

Prompts to Help You if You’re Stuck

If you’ve never planned your financial future with another person it can be daunting to make up goals from scratch. Some prompts that may be helpful:

- Pick a date in the future (say, 15 years from now). What would you like to be true? Where do you live? What is your lifestyle like? Work backward from these fantasies to produce goals that will get you there.

- There are many categories of spending, which ones do you both NOT care about? Maybe you have no interest in traveling? Or maybe you live in an urban area and don’t want to buy a new car? Be discriminate in where you will not focus.

- Look at your past spending, is there a category that surprises you? Numbers don’t lie, if spend money on something that is a signal that, on some level, it is important to you.

- Consider health, travel, your home, experience with friends, your children/family, retirement planning. Where would you like to focus in the next few years?

Your Guide to Checking In on Your Goals

Staying aligned on your finances isn’t a one time thing. While your finances should not be something you are worrying about every single day, most advisors suggest some sort of regular check-in to make sure everything is running smoothly and to make any adjustments.

Here are some tips to set it up:

Tip #1 - Pick a cadence that works for you

Most couples do it quarterly or monthly. Our suggestion: start with monthly and put it on your calendar. Most debts and bills are paid monthly and as you lay the groundwork to become financially aligned, more frequent check-ins can help you spot trouble areas more quickly before they grow into something more consequential.

Once these meetings feel perfunctory, consider changing to quarterly if it better serves your schedule.

Tip #2 - Create a recurring agenda

As best you can, structure these check-ins so everyone knows what to expect. No one likes to get blindsided with money questions, so give everyone the space to be prepared. Just like you can add personal flourishes to your wedding, do the same for your financial check-in..

“I encourage couples to sit down and have a ‘wine night’ and review what happened that month,” says Andrea Thompson, founder of Modern Cents. Make it your own. Split a bottle of wine, do it at your favorite coffee shop, or close each meeting with something fun.

A sample agenda checklist:

- What are the balances of all our accounts and debts? How does that compare to the last time we had a check-in? Include: bank accounts, credit cards, investments, mortgages, and crypto. (A glance at your Monarch account can make this simple!)

- Were there any unexpected events or expenses that month?

- What’s working and not working about the way we have organized our finances?

- Are we making progress to our goals?

On our recent agenda, the topic was to decide to send our child to public school vs private school,” says Jonathon Wong. “We discussed the additional expense of private school and determined that we wanted to use the extra cost towards her 529 to save for college instead of private school. We figured the compound interest of investing would go a long way.’”

Optional: Create a “big topics” calendar. Especially if you’re early in the relationship, it can be daunting to tackle all of the weighty money questions at once. If it’s not urgent, you can assign each monthly check-in a topic. Example monthly topics may include:

Getting all of your insurance in order

Auditing all of your recurring expenses to see if you still are using them

Planning for the year’s travel and big trips

Tip #3 - Blow it up if it doesn’t work for you

Your check-ins shouldn’t feel like a drag. If you find yourself skipping the check-ins and not communicating with your partner it’s time to reconsider your approach. Don’t be afraid to change up the frequency, venue, or agenda.

A Goal Setting Checklist

Ready to start setting goals with your partner? Here’s a handy checklist you can follow:

- Take a diagnostic or speak to a financial planner to better understand your own money personality and money beliefs.

- Enter in your current account, asset, and debt balances into a tool like Monarch so you can see where you stand.

- Write down your 1, 5, and 10 year goals.

- Ask your partner to do the above two steps.

- Compare results.

- Create SMART goals from your exercise that you will follow as a couple. Write them down.

- Schedule monthly check-ins with your partner.

- Have your first check in.

After three months: Are your goals and check-ins working for your household? If yes, continue. If not, address.