Inflation has been making big headlines recently. But unless you’re over 50, there’s a good chance this is the first time you’ve experienced high inflation as an adult. In fact, the last prolonged period of high inflation in the U.S. ended in 1991. And although there’s not much you can do to impact inflation, there are steps you can take to protect your finances.

Inflation makes your money worth less over time: As of April 2022, inflation hit 8.5% which is the highest it’s been in 40 years. That means prices are 8.5% more expensive on average than they were just a year ago. And although an 8.5% increase in prices might not sound that scary, if inflation continues at this rate, prices will double in less than 10 years and quadruple in less than 20 years. The money you have today would lose half of its value within 10 years. A $3 cup of coffee today would cost more than $6 within a decade and $12 within two decades. So what can you do to protect your finances from the impact of inflation?

You can preserve your purchasing power by looking for growth and interest. At a high level, when inflation ramps up, you can preserve your purchasing power by finding growth opportunities for your assets. If your assets are growing at the same rate as inflation, you’ll be able to buy about the same amount of stuff in the future as you can today. If your assets grow faster than inflation, you’ll have more purchasing power in the future. And if your assets grow more slowly than inflation, you're losing purchasing power over time.

Growing your assets typically means taking on risk. For money that’s earmarked for longer term goals, investing in stocks, real estate and commodities can help your portfolio keep pace with inflation and, ideally, grow faster than inflation. But for money earmarked for short term goals or set aside as an Emergency Fund, it’s typically too risky to invest those dollars given that investing brings the potential for loss.

There are limited options available to grow your savings at minimal risk. With high yield savings accounts, CDs, and most bonds paying very little interest, it’s challenging to find opportunities to grow your cash while minimizing risk. But there is one lesser known option that could be a great choice for you - Series I Savings Bonds. (The “I” stands for “inflation”.) Below, we’ll dig into what I bonds are, how they work, and some considerations as you decide whether they might be a good fit for you.

Series I bonds could help you protect your purchasing power with minimal risk. I bonds are savings bonds issued by the U.S. government. They are non-marketable, which means they aren’t bought and sold on the secondary market. Rather, they are issued directly from the U.S. government, earn monthly interest, and are eventually redeemed at full purchase price plus interest, directly from the U.S. government.

Series I bonds pay an interest rate linked to inflation. The interest rate paid on I bonds is directly linked to the Consumer Price Index for all Urban Consumers (CPI-U) which means that the interest rate is directly tied to inflation. If inflation is low, the interest rate paid on I bonds is low. If inflation is high, as it is today, the interest rate paid on I bonds is also high. In fact, I bonds purchased between November 2021 and April 2022 have an initial annualized interest rate of 7.12%, and bonds purchased between May 2022 and October 2022 are expected to pay an even higher rate given the continued increase in inflation.

The interest rate on I bonds resets every six months, in May and November, based on the current rate of inflation. The I bond interest rate at the time of purchase will apply for the first six months you own the bond, and it will reset every six months to whatever the current I bond interest rate is at each six month interval. The interest rate could certainly go down over time if inflation subsides, but will never be less than 0%. And if inflation is persistent, the interest rate will remain attractive.

Interest on Series I bonds is exempt from state and local income tax. Interest on I bonds is subject to Federal income tax, but not state or local income tax. And you get a choice on when to pay the taxes on I bonds. You can either report the interest for tax purposes every year, or you can defer reporting the interest until the earliest of the following:

You cash in your bond

You change the ownership of your bond

The bond reaches final maturity after 30 years

Series I bonds are illiquid for the first year. It's important to note that I bonds are illiquid for the first 12 months that you own them, which means you can’t redeem them and get your money back for the first year.

After the first 12 months, you can cash in your I bonds any time and get your original purchase price back plus interest earned. However, if you redeem them within the first two to five years, you’ll lose your last three months of interest.

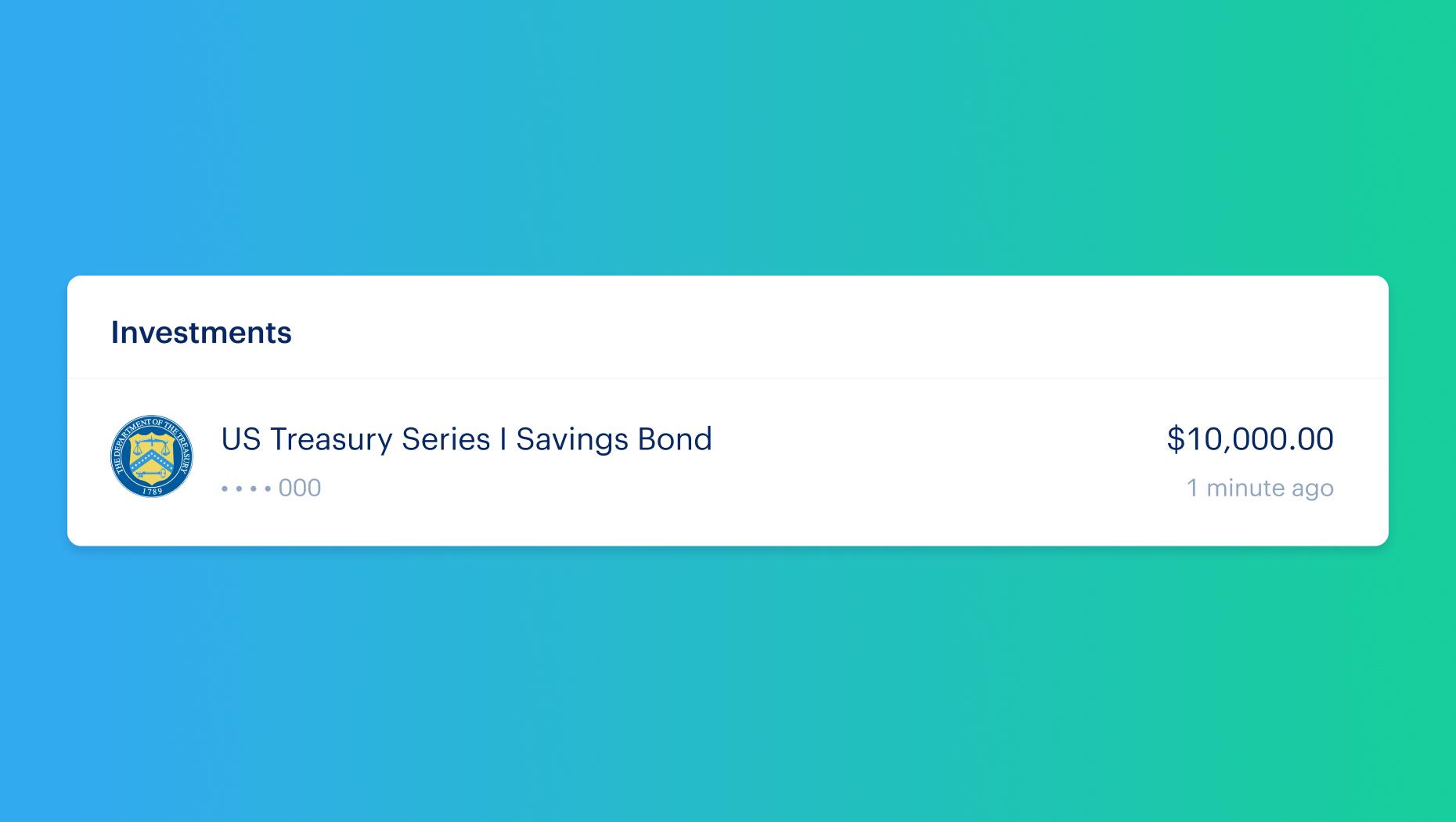

There are limits on how much you can invest in Series I bonds each year. You can purchase up to $10,000 of I bonds per person, per year, directly from the US Treasury. You can also purchase I bonds as gifts which might make sense for minor children. In addition to the $10,000 per person per year limit, you can use up to $5,000 of your tax return annually, per person, to purchase additional I bonds.

Series I bonds don’t get much attention from financial services companies because they can’t make money on selling them. At this point, you might be wondering why you’ve never heard about I bonds before. There are a couple of reasons. First, inflation has been mild for most of the last 40 years so I bonds haven’t been newsworthy. Second, I bonds are purchased directly from the government with no intermediary which means there are no commissions, sales charges, asset management fees, or money to be made on the sale of I bonds. Unfortunately, with no financial incentives to “sell” I bonds, and with competing products and services to sell instead, financial services companies tend to give I bonds much less publicity than they deserve.

Series I bonds provide a great opportunity to earn interest on cash balances, but it’s important to consider whether they’re right for you given your financial situation and your goals.

Series I bonds could help you make progress on your goals and protect your purchasing power. I bonds could be a great option if you’re certain you won’t need the cash for at least 12 months and you’re looking to:

Earn interest on cash set aside for a goal that’s one to five years away

Add some higher yielding bonds to your non-qualified portfolio (i.e. the portion of your portfolio that’s in individual, joint, or trust ownership)

Earn interest on a portion of your Emergency Fund

Put aside funds for a child that won’t be needed for at least a year

Depending on your circumstances, Series I bonds may not be the right choice. I bonds may not be a great option for you if:

There’s a chance you’ll need the cash within 12 months

You have debt at an interest rate higher than I bonds are paying

You’re looking to invest inside of an IRA, Roth IRA, 401(k) or 529 plan, as I bonds are not available for purchase within retirement and education accounts

You don’t have a Social Security number

You aren’t a U.S. citizen, U.S. resident, or civilian employee of the U.S.

Protecting your finances against rising inflation is important, but keep in mind that inflation rates will change over time, especially as the Fed raises interest rates to combat inflation. Don’t let inflation protection become more important than sound financial decisions like building your savings and keeping it safe, investing for the future, and paying down debt.

If you found this helpful drop us a note at [email protected] to let us know what you think we should write about next! Sign up now to sync your holdings & compare your portfolio performance to key benchmarks in Monarch.

No Content can or should be construed as professional advice of any kind (including financial planning, business, employment, investment, accounting, tax, and/or legal advice). The Content is provided for educational purposes only, and is not intended to be a substitute for the professional advice of a financial planner, financial advisor, accountant or otherwise.